This brings my total holdings to a grand total of 3000 units - still small but significantly larger position. I estimate this bringing up indicative dividends up by about... 2.3x - 2.5x while they are distributing 100% of distributable income up till end of FY19 (as per their policy shared in prospectus back then).

* Calculated based on 1 EUR = 1.57 SGD

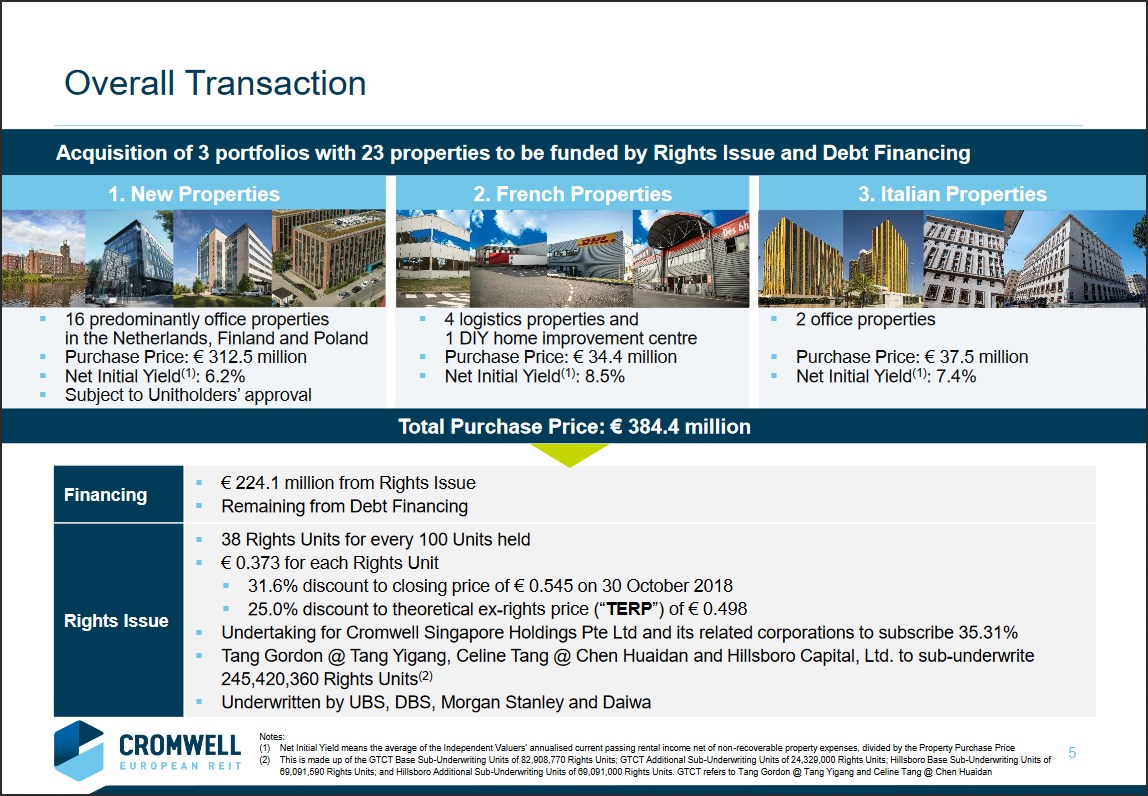

This came as a pleasant surprise for me as I do not expect to get all 2000 units. My last rights issue purchase was for Cache Logistic Trust, and even that was oversubscribed by about ~100%. It seems that this particular rights issuance was only ~5% oversubscribed.

Despite the increasing interest rate environment, DPU-dilutive effect of the purchase and the need to focus on paying off my borrowings or building up my emergency funds, I felt this was too necessary of an opportunity to pass up. It is icing to the cake that I get to pay $2 instead of $30 in commission to re-build my income portfolio. Heck, if I was in a better financial position, I would apply for a few thousand more excess rights units.

With that, although the this quarter has yet to come to an end, I update my portfolio for 4Q2018.

Income Portfolio

| |||||

Counters

|

Units

|

Market Price (SGD)

|

Overall Value based on market price (SGD)

|

Allocation

| |

1

|

Cromwell European REIT

|

3000

|

0.667*

|

2001

|

13.80%

|

Growth Portfolio

| |||||

Counters

|

Units

|

Market Price (SGD)

|

Overall Value based on market price (SGD)

|

Allocation

| |

2

|

Alliance Mineral Assets (AMAL)

|

50000

|

0.25

|

12500

|

86.20%

|

Cash and other Assets

| |||||

Counters

|

Units

|

Market Price (SGD)

|

Overall Value based on market price (SGD)

|

Allocation

| |

3

|

Warchest

|

1

|

0

|

0

|

0.00%

|

Total SGD

|

14501

|

100.00%

|

* Calculated based on 1 EUR = 1.57 SGD

Wishing everyone a Merry X-mas (or otherwise Happy Holidays) in advance!