Introduction

Cromwell European REIT (SGX: CNNU) is a SGX-listed REIT that holds a portfolio of largely Office Properties based in Europe. It had successfully IPO-ed on its second attempt to list towards end of after adjusting the portfolio and the offering. Its sponsor is Australia-listed Cromwell Property Group. It trades in EUR dollars (for people investing with CPF-OA, you can't buy with CPF unless it's priced in SGD). The trust issues distribution semi-annually and intends to issue 100% of distributable income till FY2019.

Distribution

Its maiden distribution for period of 30 November 2017 to 30 June 2018 (7 months instead of 6 months) was paid out at EUR 0.0253 (SGD 0.04031) per unit. If we convert this to a semi-annual payment, it translates to EUR 0.02168 (SGD 0.03455) per unit. Based on its last traded price of EUR 0.545 as at 2nd November 2018, this translates to an annualised distribution yield of ~7.92%.

Share Price Movement

Looking at YTD Chart, price has been on the decline since its peak of SGD 0.635 on 17 May 2018. This is in line with Straits Time Index as well, which has been on a decline since its peak of 3615.28 on 02 May 2018.

|

| Source: SGInvestor.io |

|

| Source: Yahoo! Finance |

Interestingly, there has been some increased short selling going on (link to price movement on SGInvestor.io here) - looks like some traders are taking advantage of pessimism from the rights issue. The rights issue will cause weakness on its price for a while on top of interest rate hike, probably continuing to present headwind to the share price as with a lot of REITs out there.

The past few trading sessions have started to turn positive so after once it hits support and if the positive momentum of the market is sustained, that could mean the stock will find support not too far off that may allow slight rebound in price.

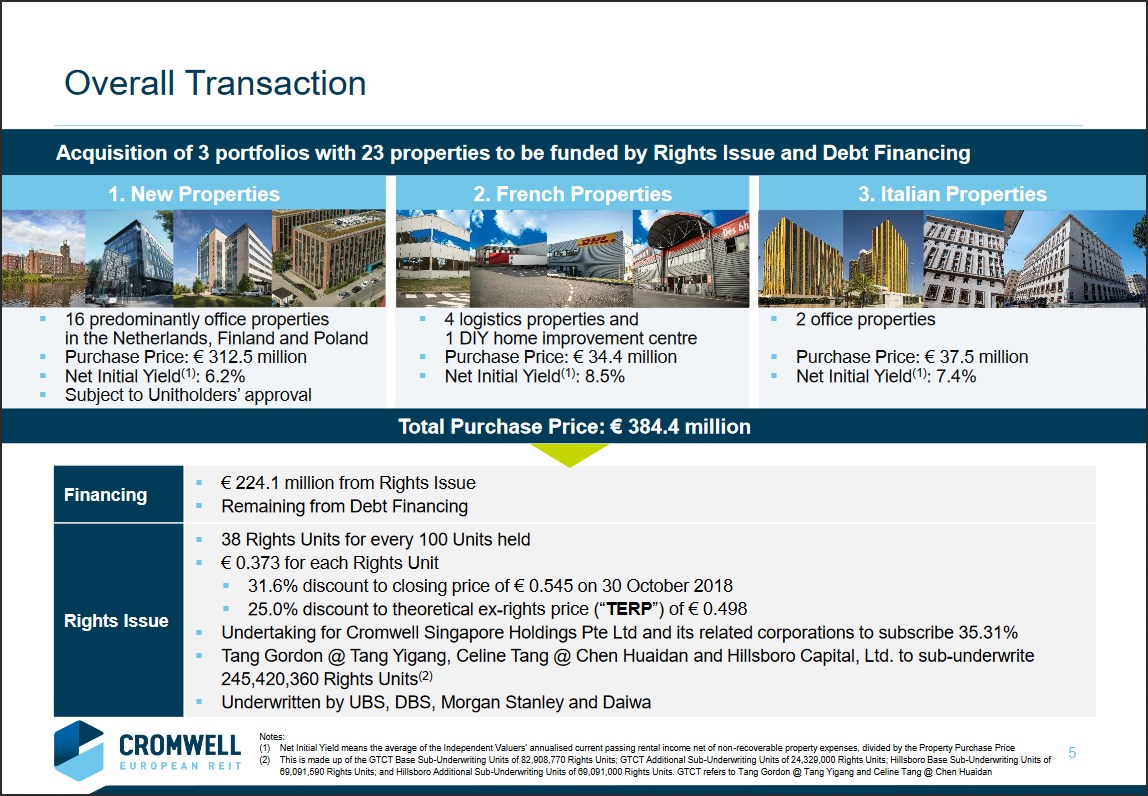

Rights Issue

On 30th October 2018, the trust had announced acquisition of 3 portfolios totalling 23 properties and intend to fund the acquisition partially via raising approximately EUR 224.1m by means of a 38-for-100 rights issue (remainder via debt financing). Altogether there will be 600,834,459 units at EUR 0.373 per unit up for offer in this rights issue. (link here). The acquisition and rights issue is subject to shareholders' approval during the EGM to be held on 15 November 2018 (Thursday) at PARKROYAL at Pickering.

|

| Source: Cromwell European REIT |

- Undertaking for Cromwell Singapore Holdings Pte Ltd and its related corporations to subscribe 35.31% for the rights issue. This is significant to me as they will maintain no drop in % of ownership of the share and hence can be interpreted as a vote of confidence.

- As of present, total share base is 1,581.14m. Post-rights issue, the total share base will be increased to 2,181.98m (enlarged by 38%).

- Theoretical ex-rights price (TERP) of EUR 0.498 assuming full and proportionate subscription by all shareholders means averaging down from current price by 9% (hardly the case though...).

- Based on theoretical forecast of distribution, total distributable income is expected to increase by ~22%.

- Taking into account the enlarged share base, this could translate to a theoretical reduction in DPU by 12%.

- CEREIT's current gearing is 36.8%. Since the acquisition will also be funded by debt financing, gearing will go up.

- A quick glance through the rights offering presentation slides reveals some properties have a short Weighted Asset Lease Expiry (WALE) (some are even only a month away from expiry!), so that may be a concern to some investors.

Disclaimer: The above (especially my own observations) should not be used as a decision to solicit buy/sell activity. Use all information at your own discretion and DYODD.

No comments:

Post a Comment